Quick Answer

Value betting means placing bets where your estimated probability of an outcome is higher than the probability implied by the bookmaker’s odds. When you consistently find and back bets where the price is better than the true likelihood warrants, you have a mathematical edge. That edge — expressed as positive expected value — is what separates the small number of long-run profitable sports bettors from the majority who lose. Value betting is not about picking winners. It’s about finding prices that are wrong.

Introduction

Most sports bettors think about betting the same way. Pick the team most likely to win. Back them. Repeat. It sounds logical. It’s also why roughly 97% of sports bettors lose money over the long run. Not because they’re bad at predicting outcomes — but because picking likely winners and finding value are two completely different activities.

A team that wins 70% of their games offers zero value at odds implying 80% probability. A team that wins 40% of their games represents excellent value at odds implying only 25% probability. The quality of a bet has nothing to do with how likely the outcome is in isolation — it has everything to do with whether the price is right relative to the true probability.

This is value betting. It’s the foundation of every profitable sports betting approach that has ever existed. Without it, you’re just paying entertainment tax to the bookmakers at a rate they set. With it, you have a genuine mathematical framework for long-run profitability.

This guide explains what value betting is, how to find it, how to measure whether you’re doing it correctly, and what it actually takes to sustain an edge in modern sports betting markets.

What Is Value in a Bet?

Value exists when the price you’re offered is better than the true probability of the outcome.

That requires two things: a price (the odds), and a probability assessment (your estimate of the real likelihood of the outcome). The gap between those two things — if one exists — is the value.

“Value betting is not about being right. It’s about being right at better odds than the market thinks you should be.”

Let’s make this concrete with a simple example.

You’re offered 2.50 decimal odds on a tennis player winning a match. Convert that to implied probability: 1 ÷ 2.50 = 40%. The bookmaker’s price says this player has a 40% chance of winning.

After your own analysis — head-to-head record, current form, surface statistics, injury reports — you estimate this player’s actual probability of winning at 52%.

That gap between 40% (bookmaker’s implied probability) and 52% (your estimate) is where the value lives.

The expected value calculation confirms it:

EV = (0.52 × £1.50 profit) − (0.48 × £1 stake) = £0.78 − £0.48 = +£0.30

For every £1 staked on this bet, you expect to return +30p over time — if your probability estimate is correct.

If. That qualifier matters enormously, and we’ll come back to it.

How Bookmakers Build Their Margins

To find value consistently, you need to understand exactly how bookmakers price markets — because the margin they build in is the primary obstacle you’re trying to overcome.

The Overround (Vig)

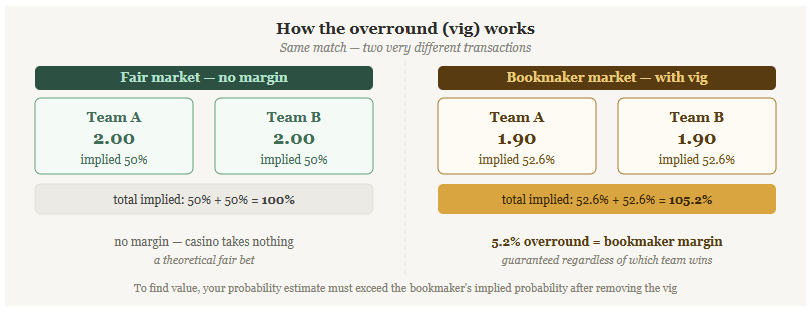

When a bookmaker prices a two-outcome market — say, Team A vs Team B — they don’t simply reflect true probability. They add a margin, known as the overround or vig, to ensure they profit regardless of which side wins.

Here’s a simplified example. The true probability of a match might be:

- Team A wins: 50%

- Team B wins: 50%

A fair market would offer both sides at 2.00 (evens). But a bookmaker offering 2.00/2.00 makes no profit — they’re simply taking money from one group of bettors and handing it to the other.

Instead, they might offer:

- Team A: 1.90

- Team B: 1.90

Converting to implied probabilities: 1/1.90 = 52.6% for each side. Added together: 105.2%. That extra 5.2% is the overround — the bookmaker’s guaranteed margin embedded in the market.

To make a profit on this market, a sports bettor must overcome that 5.2% margin before variance has any influence. On a single bet, that might not sound difficult. Accumulated across thousands of bets at losing probability, it’s a mathematically robust barrier.

How the Vig Varies

The overround is not fixed. It varies by:

- Sport: Major football markets typically carry a vig of 4–6%. Niche markets — lower league football, minor tennis events — often carry 8–15%.

- Market type: Match result markets carry lower margins than corners, bookings, or first goalscorer markets.

- Bookmaker type: Soft books (recreational-facing operators) carry higher margins. Sharp books and betting exchanges carry lower margins.

This matters for value betting. Lower-margin markets provide a lower bar to clear before finding genuine +EV opportunities. Chasing value in heavily juiced markets is starting from a harder position.

Sharp vs Soft Bookmakers

Understanding the distinction between sharp and soft bookmakers is fundamental to value betting.

Soft books — major recreational operators — often open lines early, adjust based on bet volume rather than sharp money, and carry higher margins. Their opening lines can be less efficient, creating more value opportunities. However, they actively limit and restrict identified winning customers.

Sharp books — Pinnacle being the best-known example — price markets more accurately, carry lower margins, and accept large bets from winning players. Their closing lines are widely considered the most accurate market prices available.

The gap between a soft book’s opening line and a sharp book’s closing line is often where value is found and confirmed.

How to Find Value Bets

Finding genuine value in sports betting requires a process. Not a system. Not a shortcut. A disciplined analytical process applied consistently across a large number of bets.

Step 1: Build Your Own Probability Estimate

Before looking at any odds, form an independent view of the true probability of each outcome.

This is the most important — and most difficult — step. Your probability estimate needs to be better calibrated than the bookmaker’s for value to exist. That requires:

- Statistical analysis: Team and player performance data, form, head-to-head records, home/away splits, situational factors

- Contextual awareness: Injuries, suspensions, lineup changes, motivation factors, travel schedules

- Market understanding: Where public money is biasing the line away from true probability (more on this below)

The key discipline: form your probability estimate before checking the odds. Once you see a price, it anchors your thinking. Independent probability assessment requires removing that anchor.

Step 2: Convert Odds to Implied Probability

Once you have your estimate, convert the available odds to their implied probability for comparison.

Decimal odds to probability: 1 ÷ decimal odds

- 2.00 = 50%

- 1.80 = 55.6%

- 3.50 = 28.6%

Fractional odds to probability: denominator ÷ (numerator + denominator)

- 5/2 = 2 ÷ 7 = 28.6%

- Evens (1/1) = 1 ÷ 2 = 50%

American odds to probability:

- Negative odds (favourites): |odds| ÷ (|odds| + 100) → −150 = 150/250 = 60%

- Positive odds (underdogs): 100 ÷ (odds + 100) → +200 = 100/300 = 33.3%

Always remove the overround before comparing. A simple approach: convert all outcomes to implied probability, add them up, then divide each by the total. This gives you the book’s “devigged” probability — the true price they’re implying without the margin.

Step 3: Compare Your Estimate to the Market Price

If your estimated probability of an outcome is higher than the market’s devigged implied probability, the bet has positive expected value — assuming your estimate is correct.

| Your Probability Estimate | Market Implied Probability | Value Status |

|---|---|---|

| 55% | 40% | ✓ Strong value |

| 50% | 48% | ✓ Marginal value |

| 45% | 45% | ✗ No value (break-even) |

| 40% | 50% | ✗ Negative value |

| 30% | 45% | ✗ Strongly negative |

The size of the edge matters as much as its existence. A 2% edge is real but requires very high volume before it becomes statistically distinguishable from luck. A 10%+ edge is meaningful and detectable in lower samples — but also increasingly rare in efficient markets.

Step 4: Bet Sizing — Proportional to Edge, Not Confidence

Once you’ve identified a value bet, how much you stake matters enormously.

The mathematically optimal staking approach is the Kelly Criterion: stake a fraction of your bankroll proportional to your estimated edge.

Kelly fraction = (bp − q) ÷ b

Where:

- b = decimal odds − 1 (your profit per unit staked)

- p = your estimated probability of winning

- q = 1 − p (your estimated probability of losing)

A bet with 5% edge at decimal odds of 2.00: Kelly fraction = (1 × 0.55 − 0.45) ÷ 1 = 10% of bankroll

In practice, most professional value bettors use fractional Kelly — staking 25–50% of the full Kelly recommendation. This reduces variance dramatically while preserving most of the long-run growth rate. Research from the Wharton School found that full Kelly led to bankruptcy in 100% of simulated scenarios in realistic betting environments, while partial Kelly with a 0.50 coefficient was the most practical strategy for limiting variance while still capitalising on positive EV opportunities.

Closing Line Value: The Professional’s Yardstick

Ask any professional sports bettor how they measure performance and most will give the same answer: Closing Line Value (CLV).

CLV is the single most important metric in value betting — and the one most recreational bettors have never heard of.

What Is Closing Line Value?

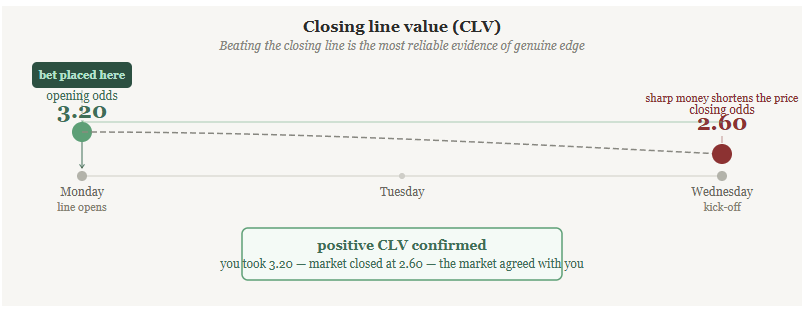

Closing line value is the difference between the odds you took and the odds available at market close (just before the event starts).

The closing line is considered the most accurate price available. As the event approaches, sharp money, public volume, and information flow converge to push the market toward its most efficient state. The closing line reflects the collective wisdom of the most informed bettors in the world.

If you consistently bet at better odds than where the market closes, you’re demonstrating genuine predictive ability. You’re finding mispricings that the market later corrects.

“Beating the closing line consistently is the only reliable evidence that you’re actually finding value — not just running hot.”

A CLV Example

You back a football team at 3.20 on Monday morning, two days before the match.

By kick-off on Wednesday, the same team has been bet down to 2.60 by sharp money and informed public betting.

Your opening price of 3.20 is significantly better than the closing 2.60. You have positive closing line value. The market moved in the direction your analysis predicted — and that movement is evidence of genuine edge, not luck.

If the result had gone against you, it wouldn’t change the fact that the bet had value at 3.20. The quality of a value bet is determined at the time it’s placed — not by the outcome.

Why CLV Matters More Than Results

Short-run results in sports betting are dominated by variance. A bettor with genuine edge can lose money for weeks or months purely due to normal statistical fluctuation. Conversely, a bettor with no edge can profit for weeks or months on the same variance — and often mistakes it for skill.

CLV cuts through that noise. If you’re consistently beating closing lines, you’re finding real value. If you’re not, the profits you’re experiencing are likely variance that will eventually normalise.

Tracking CLV on every bet is the professional discipline that separates analytical bettors from everyone else. It requires recording not just the result, but the opening odds taken and the closing odds for every bet placed.

Where Value Comes From: Market Inefficiencies

The existence of value in a sports betting market requires the market to be wrong — at least temporarily. Understanding where and why markets misprice outcomes is essential to finding genuine edge.

Public Bias and Sharp Money

Bookmakers don’t just model probabilities. They also manage their liability — the risk of paying out on one-sided action.

When a large proportion of recreational bettors favour one team, books often shade their lines toward that team — offering slightly worse odds on them and slightly better odds on the opposition. This creates temporary value on the other side of popular public money.

Identifying when a line has moved for liability reasons rather than informational reasons is a core skill of professional sports bettors. A line that opens Team A at 1.85, attracts heavy public money, and moves to 1.70 has likely moved for liability reasons. The opposition at improved odds may represent value.

Recency Bias and Narrative Markets

Markets — and the bettors who move them — are susceptible to recency bias. A team that lost three consecutive matches gets underestimated. A team on a winning run gets overestimated. The public prices narratives more than probabilities.

This creates exploitable mispricings in markets where:

- A team’s recent form is highly visible and unusual

- A prominent player has recently returned from injury or scored a hat-trick

- Public sentiment is running strongly in one direction based on recent events

Systematic analysis that weights long-run performance correctly — rather than overweighting recent results — can find value in these situations.

Opening Lines vs Closing Lines

The gap between opening and closing lines represents the market’s correction process. Opening lines are less efficient than closing lines — they’re set by a smaller number of analysts before the full information set and sharp money has been applied.

Professional value bettors often target opening lines precisely because of this. Being first into the market with a correct probability assessment is where edge is most reliably captured. By the time casual bettors are placing their wagers, the market has often already moved toward efficiency.

Niche and Emerging Markets

Major markets — Premier League match results, top-flight NFL point spreads — are highly efficient. Significant sharp money and sophisticated modelling continuously pushes prices toward accuracy. Finding sustained edge in the most liquid, most-watched markets is exceptionally difficult.

Niche markets offer more opportunity:

- Lower-league football, where data is thinner and model accuracy more varied

- In-play markets, where the speed of line adjustment creates temporary mispricings

- Player proposition markets, where public attention is lower

- Early-season markets, where team strength is less established

This doesn’t mean niche markets are easy. But the efficiency gap is wider, and there are fewer professional eyes competing for the same edge.

The Practical Reality of Sustaining Value Betting Edge

Here’s where honesty matters most — and where most sports betting content falls down.

Most Bettors Cannot Sustain Positive CLV

Finding value consistently is genuinely difficult. The modern sports betting market is more efficient than at any point in its history. Algorithms, data analytics firms, professional syndicates, and sharp books operate with enormous computational resources and data advantages over individual bettors.

The bar for consistent positive CLV has never been higher.

Estimates vary, but approximately 2–5% of sports bettors sustain positive ROI over the long run. The rest lose at a rate determined by the vig they’re paying.

This is not a reason not to try. It’s a reason to be honest with yourself about whether the edge you think you have is real, or whether you’re experiencing variance.

Sportsbooks Actively Limit Winners

Even genuine positive-expectation bettors face a structural problem with no equivalent in casino gaming: sportsbooks limit and ban winning customers.

Recreational-facing operators — the books offering the most accessible margins and the most line inefficiencies — are also the most aggressive at limiting profitable bettors. A bettor consistently beating the market at a major UK book may find their maximum stake reduced from £200 to £5 within weeks.

This creates a real ceiling on monetising genuine edge:

- The books where value is most available are the quickest to limit winners

- Sharp books that accept winners (Pinnacle, Asian books, betting exchanges) have more efficient lines with less margin to exploit

Exchanges like Betfair offer a partial solution — you’re betting against other bettors, not the house, and winning bettors are not limited. The commission (typically 2–5% of net winnings) replaces the vig, but a sufficiently skilled bettor can sustain positive expectation even after commission.

The Sample Size Problem

Value betting edge only becomes statistically visible over large samples. At 5% ROI and typical odds of around 2.00, you’d need approximately 1,000+ bets before your results become statistically distinguishable from a break-even bettor at the 95% confidence level.

Most bettors never play enough volume for their edge — or lack of edge — to become clear. They operate in perpetual short-run noise, mistaking variance for skill in both directions.

This is why tracking CLV is so important. CLV provides a faster, more reliable signal of genuine edge than results alone — because market efficiency is your benchmark rather than variance-dominated outcomes.

Pros and Cons: Value Betting as a Strategy

| Pros | Cons | |

|---|---|---|

| Mathematical foundation | Grounded in probability and EV | Requires accurate probability estimation — hard to do consistently |

| Long-run profitability | Theoretically possible for skilled analysts | Only ~3–5% of bettors sustain positive ROI long-term |

| Measurable performance | CLV provides objective performance feedback | Requires detailed tracking discipline |

| Works across sports | Applicable to any sport with odds markets | Some sports/markets are more efficient than others |

| Scalable approach | Can be applied systematically at volume | Winners are limited by most major operators |

| No house edge ceiling | Unlike casino games, not mathematically fixed | Still requires beating a significant vig |

Expert Insight: How Professional Value Bettors Think

The mindset shift between recreational betting and professional value betting is more significant than the analytical shift.

Professionals don’t ask “who will win?” They ask: “What is this outcome’s true probability, and is the available price better or worse than that probability warrants?” These are not the same question. A team that wins 70% of the time is still a bad bet at odds implying 85%.

Professionals treat every bet as a long-run policy, not a single event. When you decide to back a value bet at 3.20, you’re not making a decision about this match. You’re making a decision about what to do every time an analogous situation presents itself. The question is whether that policy makes money over 1,000 similar decisions — not whether it wins this one.

Professionals separate the bet quality from the result. A +EV bet that loses is still a good bet. A −EV bet that wins is still a bad bet. The only thing that should inform whether you take a bet again is whether your probability estimate was well-founded — not whether the last one won.

Professionals track everything. Every bet logged: the sport, the market, the odds taken, the closing odds, the result, the CLV, the stake. Without data, you cannot distinguish genuine edge from variance. With data across 500+ bets, the picture starts to become clear.

Professionals manage bankroll with explicit rules. Fractional Kelly staking, fixed unit sizes, or percentage-of-bankroll approaches — the method matters less than the consistency. Chasing losses, increasing stakes after wins, or bet sizing based on confidence rather than edge are all patterns that destroy long-run profitability regardless of how good the underlying analysis is.

Building a Value Betting Process

A practical framework for bettors who want to approach this seriously:

1. Choose Your Sports Carefully

Specialise. The more deeply you understand a sport, a league, or a specific market, the more likely your probability estimates will be better than the market’s. A bettor who follows a single lower-league football division obsessively is more likely to find genuine edge there than across ten sports they follow casually.

2. Build a Simple Model

You don’t need machine learning or a PhD. A spreadsheet tracking team performance metrics — goals scored/conceded, expected goals (xG), home/away splits, form — gives you a systematic basis for probability estimation that outperforms intuition alone.

3. Line Shop Aggressively

Always take the best available price. A consistent 0.1–0.2 improvement in average odds across hundreds of bets has a significant impact on long-run ROI. Use multiple accounts across different books to compare prices before placing every bet.

4. Track CLV on Every Bet

Record the odds you took and the closing odds for every bet. Review this data monthly. If your average CLV is positive — you’re consistently beating closing lines — that’s evidence of genuine edge. If it’s negative or flat, the analysis needs reassessing before conclusions are drawn.

5. Set Explicit Bankroll Rules

Decide your staking approach before you start. Stick to it. The psychological pressure of a losing run tempts even disciplined bettors to deviate — to bet bigger to recover, or to abandon the approach entirely. The staking rules exist for exactly those moments.

Responsible Gambling

Value betting is an analytical discipline, not a reliable income source. The honest reality is that most people who attempt value betting will not sustain positive ROI — either because the edge they believe they have isn’t real, because they don’t have sufficient volume or tracking discipline to measure it accurately, or because operator restrictions limit the ability to act on genuine edge.

No betting strategy guarantees profit. Even professional bettors with genuine, documented positive CLV experience extended losing runs due to normal variance. Past profitability does not guarantee future results.

Gambling should remain a recreational activity with clearly defined financial limits. If betting is generating financial stress, influencing decisions it shouldn’t, or feeling compulsory rather than enjoyable, that’s a signal to take seriously. Every regulated gambling provider offers deposit limits, session limits, time-outs, and self-exclusion — free tools that work, available immediately.

FAQ

What is value betting in simple terms?

Value betting means backing an outcome when the odds offered are better than the true probability of that outcome occurring. If you estimate a team has a 55% chance of winning, and the odds imply a 40% probability, that bet has value — regardless of whether you win or lose on this particular occasion.

How do I calculate if a bet has value?

Convert the odds to implied probability (1 ÷ decimal odds). Compare this to your own probability estimate. If your estimate is higher than the implied probability, the bet may have positive expected value. Multiply your estimated probability by the potential profit, subtract the probability of losing multiplied by the stake, and the sign of the result tells you whether the bet is positive or negative EV.

What is closing line value and why does it matter?

Closing line value (CLV) is the difference between the odds you took and the odds at market close. Bookmakers’ closing lines are the most accurate prices available — they reflect all available information and sharp money. Consistently taking odds better than where the market closes is the most reliable indicator of genuine value betting skill, because it demonstrates predictive ability independently of short-run results.

Can you make money from value betting long-term?

Theoretically yes. In practice, only a small fraction of bettors — estimated at 2–5% — sustain positive ROI over large sample sizes. The barriers are significant: forming accurate probability estimates better than the market, dealing with operator restrictions on winning customers, and maintaining the volume and discipline required for edge to become statistically visible.

Why do bookmakers limit winning customers?

Recreational-facing bookmakers are not in the business of accepting informed bets at a disadvantage. When a bettor demonstrates consistent positive CLV — taking prices that the market subsequently corrects — they represent a liability rather than a recreational customer. Limiting stakes or closing accounts is how soft books protect their margins from advantage players.

Is value betting different from matched betting?

Yes. Matched betting exploits bookmaker promotional offers (free bets, enhanced odds) to lock in profit by covering all outcomes. It’s a specific technique based on offers rather than analytical edge. Value betting is about finding genuine mispricing in standard markets through probability analysis. Both can produce positive returns — but value betting is a long-run analytical skill, while matched betting is an arbitrage technique that exhausts available offers over time.

How many bets do I need before I know if my value betting is working?

A meaningful assessment requires a minimum of 500–1,000 bets tracked with full CLV data. At lower sample sizes, variance creates too much noise to distinguish genuine edge from luck. Even at 500 bets, statistical confidence is limited. This is why CLV is so important — it provides a better signal than results alone at lower sample sizes, because it’s benchmarked against market efficiency rather than variance-dominated outcomes.

Conclusion

Value betting is the only mathematically coherent approach to sports betting. Everything else — backing favourites, following tipsters, chasing hot streaks, applying staking systems — is either equivalent to or worse than finding bets where the price is genuinely better than the true probability.

But honest appraisal matters. Finding consistent value in modern sports betting markets is genuinely difficult. The market is efficient, operators restrict winners, and the sample sizes required before edge becomes statistically visible are larger than most bettors ever reach.

What value betting offers is a framework — a way of thinking about every bet as an EV calculation rather than a guess, and a way of measuring performance through CLV rather than short-run results. That framework is useful even for recreational bettors who never turn professional, because it replaces intuition with analysis and replaces hope with probability.

The bettors who do it well don’t win every bet, every week, or even every month. What they do is make decisions that are justified by the maths — and measure their performance against a benchmark that reflects reality rather than variance.

That, more than any single bet, is what finding edge against the market actually means.

Related Reading

- What Is Expected Value in Gambling?

- What Is the House Edge and How Does It Work?

- Can Skill Overcome the House Edge?

- Skill vs Luck in Gambling: The Full Breakdown

- Bankroll Management: Protecting Your Money Over the Long Run

- How Professional Gamblers Think Differently

External Sources:

- Wharton School — Betting Strategy and Kelly Criterion Research

- arXiv — Optimal Sports Betting Strategies in Practice

No gambling strategy guarantees profit. All gambling carries financial risk. Past performance does not predict future results. If you have concerns about your gambling, please use the responsible gambling tools available through your provider or contact your local support service.